On March 24, 2024, the Tata Group of Industries— India’s largest conglomerate— recorded a market capitalization of $382 billion; a staggering valuation larger than the entire GDP of Pakistan ($338 billion). Within the last year, the group became the first Indian company to join Apple’s iPhone supply chain, unveiled an $11 billion investment to set up the first semiconductor fab facility in Gujarat, and introduced plans to develop an end-to-end cutting-edge chips assembly and packaging unit in Assam. Contrast the aims of India’s top group to penetrate the global high-tech manufacturing space with the colorless aspirations of one of Pakistan’s largest conglomerates, which recently announced its vision to expand its product portfolio by grabbing a further stake in the food and cereal business.[1]

In her seminal work on economic development, Alice Amsden points to the centrality of elite aspirations in shaping patterns of long-term industrial development.[2] Drawing upon a host of empirical studies from across the globe, she demonstrates that “the foundations of elite influence and the incentives they face are rooted in an economic structure which is continuously shifting”[3]. Thus, “by understanding the origins of certain elites, we gain greater insight into how different parameters change the balance of influence between groups”. [4]

How do we explain the divergent sectoral aspirations of Indian and Pakistani business groups? Why are the former vying for a greater share of the semiconductor, Artificial Intelligence, and robotics industrial space while the latter continues to operate in low-value activities? What are the prerequisites to industrial development, specifically the ‘eco-system’ (knowledge centers, universities, skill sets, R & D) that must be in place for industrial policy to work? Are private investments in some sectors more likely to succeed in one policy environment and fail in another? If actual outcomes— the sectoral winners and losers of a policy mix — can be used as a proxy for the revealed preferences of the state, a glance at Tables 1 and 2 demonstrates a fundamental fact about the two economies: of the top 10 listed companies, three are from the IT sector in India; in contrast, energy, fertilizer, and food businesses continue to dominate the imaginations of the Pakistani business landscape.

| Company | Sector |

| Reliance Industries | Conglomerate |

| HDFC Bank | Banking |

| Tata Consultancy Services | Information Technology |

| ICICI Bank | Banking |

| Bharti Airtel | Information Technology |

| Hindustan Unilever | Consumer Staples |

| Infosys | Information Technology |

| ITC | Conglomerate |

| State Bank of India | Banking |

| Housing Development Finance Corp | Banking |

Table 1: Sectoral Distribution of India’s Top 10 Listed Companies

| Company | Sector |

| OGDC | Energy |

| Meezan Bank | Banks |

| Mari Petroleum | Energy |

| Nestle | Food and Beverage |

| Colgate Palmolive | Household |

| Pakistan Petroleum | Energy |

| Pakistan Tobacco | Food and Beverage |

| MCB Bank | Banks |

| Lucky Cement | Materials |

| Engro Fertilizers | Materials |

Table 2: Sectoral Distribution of Pakistan’s Top 10 Listed Companies

As the business world looks to diversify its supply chains— a phenomenon known as the ‘China plus one business strategy’— what lessons can Pakistani policymakers learn from successful entrants into global value chains? This short essay argues that an answer must be sought in reimagining Pakistan’s industrial policy and the political economy that underpins it. Such rethinking must go beyond the archaic binaries of state versus private, free trade versus protectionism, and exchange-rate flexibility versus fixity. As Dani Rodrik points out, the discussion on industrial policy should rarely ever be about “whether the government should be involved”; rather, it should be about the how dimension.[5]

To understand why, let us ask a simple question: can the recent rise of Indian firms be seen in isolation from the will of the Indian state? Far from it. The meteoric rise of Tata, and its rapid expansion in the high-tech manufacturing space, are intricately tied with the government’s Make-in-India program and the massive amounts of financial incentives offered to sectors under the Production Linked Incentive (PLI) scheme. The PLI scheme is an initiative that offers targeted incentives to firms operating in specific sectors to “promote domestic manufacturing and reduce reliance on imports”.[6]

But the Tata Group is not the only beneficiary of the PLI scheme; a host of companies are claiming a stake in India’s future as an industrial powerhouse. This remarkable ascent is backed by a host of rising stars in the high-tech sector in 2024: Star Trace (Chennai) amassed a revenue growth of 223% in the domain of Industrial Supplies; Allied Engineering Works (Delhi) doubled its revenues in the Electronic and Electrical Goods industry, while Synnova Gears and Transmissions recorded a 43% growth spurt in the Industrial Engineering sector.

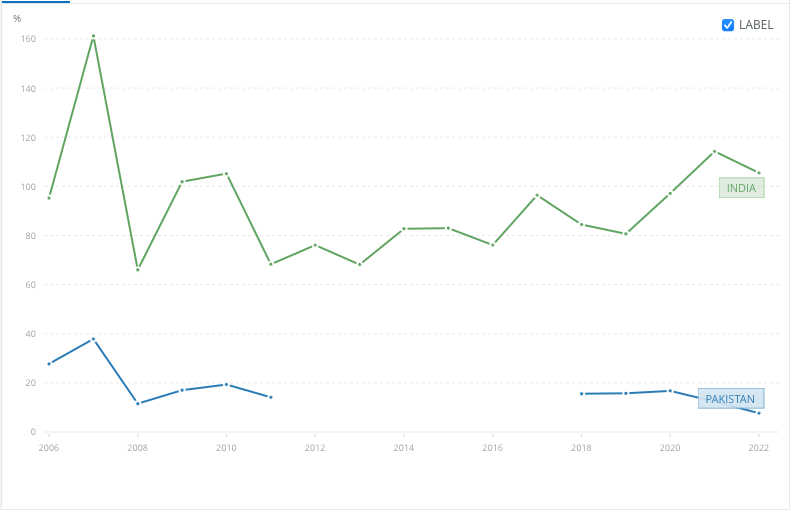

This is exactly what economic theory predicts: a networked effect of sectoral accumulation ensues when steered by appropriate targeted incentives by the state, resulting in a diffusion of economy-wide effects. As Figure 1 shows, the market capitalization as a percentage of GDP— a measure of how the valuations of publicly listed firms relate to the overall output of the economy— stands at 102% for the Indian economy. Market valuations reflect investor’s assessments of the long-term earnings potential of a business and are, as such, a measure of the cash flow generating potential of a firm on the one hand and investor’s optimism on the other. The comparable number for Pakistan is 7%. These differences must be traced back to industrial policy for reasons described below.

Figure 1: Market Capitalization of Listed Firms as % of GDP

Firstly, the financial incentives offered to companies under the PLI scheme are not a blank cheque; instead, the government adopts a carrot-and-stick approach so that “companies are incentivized based on their incremental sales of manufactured goods over a specified base year”.[7] This is critical. For instance, in the Pakistani case, fertilizer companies have benefitted enormously from input subsidies on the pretext that farmers would gain access to cheaper fertilizer. Yet, fertilizer prices on the Pakistani side continue to outstrip prices across the border. Clearly, this is a case in which the Pakistani economy would benefit from less state intervention, more free trade, less protectionism, and a redirection of precious tax-payers money toward high-performing sectors. Mubarak Ali, in an authoritative analysis of Pakistan’s fertilizer sector, runs several simulations to find that “removing the gas subsidy and investing in agricultural research will result in the highest social benefit”.[8] It is not then a question of ‘whether the state should intervene’, but rather, how, and where (i.e. which sector).

Industrial policy deals with precisely those questions. It is defined as the set of sector-specific policies that aim to direct industrialization towards the pursuit of ‘some definition of national interest.’[9] As Ha Joon Chang points out, given the fact that there are scarce resources to work with, industrial policy is always about steering the economy towards some sectors (and hence, not others). Thus, any discussion of the ‘correct mix’ of policies, that will promote industrial growth and activity must be preceded, as well as guided by a delineation of those interests via 1) an analysis of the challenges, or the set of forces obstructing industrialization, and 2) a counterfactual analysis of how similar economies have dealt with those issues.

It is crucial to appreciate the nature of the disease at the outset; whatever solution (policy mix) is proposed can then be assessed in terms of how well (or badly) it performs on those fronts. After all, a treatment plan is only as good as its ability to identify and discriminate between the causes on the one hand and its ‘symptomatic’ manifestations, on the other. While there are a host of confounding issues befuddling policymakers, three distinct, yet interrelated, sets of fundamental problems stand out as the most urgent ones and must be the immediate focus of attention:

1) Labor absorption and under-investment problem; specifically, the fact that the rate at which new entrants enter the labor market— approximated by the rate of population growth— far exceeds the rate at which the domestic economy generates quality jobs to absorb this reserve army of new workers. The symptoms of the disease? Chronically high unemployment, under-employment, and migration of high-skilled workers. Moreover, the problem creates a chicken-and-egg problem of under-investments, whereby the lack of job creation, in turn, leads to lower domestic effective demand due to the corollary that unemployed workers do not have sufficient incomes with which to buy the products produced by Pakistani capitalists, thus disincentivizing the latter to invest and produce goods profitably.

2) Non-productive consumption; specifically, the alarming tendency that over the years Pakistan has become an economy that seeks to consume without producing. As Joseph Schumpeter and Luigi Pasinestti, two of the greatest minds on structural transformation in the long run point out, an emerging industrializing economy is characterized by its ability to consume inputs productively, which means that it generates an output that can be sold to domestic or foreign consumers at a margin, that is, in a manner that produces a surplus. This surplus can then be plowed back, thus leading to structural expansion over time.

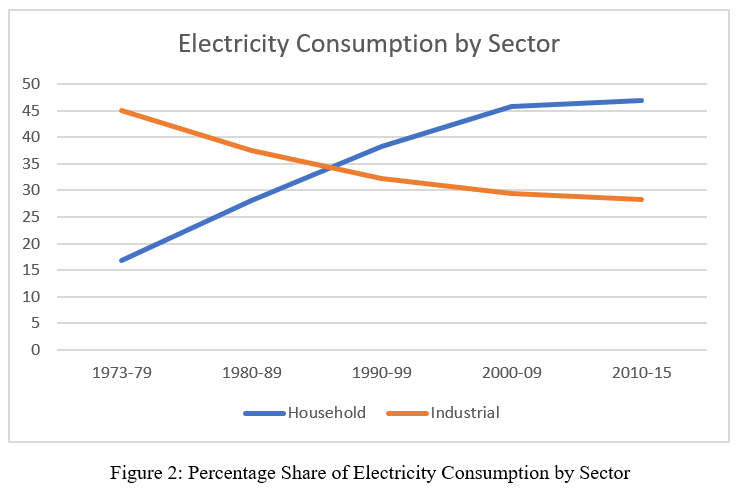

Unfortunately, Pakistan’s input consumption patterns reveal the opposite. One example (there are numerous inputs to consider) can be drawn from the sectoral patterns of electricity consumption shown in Figure 2.

In the five decades between 1973 to the present, household consumption as a share of total electricity consumption increased from 16% to 47%; the share of industry, by contrast, fell from 48% to 28%. For the sake of comparison, this sharply contrasts with India and Bangladesh, where the consumptive share of the productive sectors rose in the preceding decades and consistently remains above 45%, today. Moreover, a large share of Pakistan’s imports consists of final consumer goods, or goods that will not undergo any value addition in the domestic economy other than the marginal returns it will generate for freight, transportation, and retailing firms in Pakistan. Since no economy can sustainably keep consuming without producing an equivalent or incremental value in return, this problem manifests itself in Pakistan’s balance of payments deficits, debt crisis, and exchange-rate depreciation to name just a few of the symptoms of this disease.

3) External dependence in primary inputs. Industrial production is inseparable from the procurement and costs of the inputs that will be used up in the process. If an economy is unable to reduce its reliance on external economies for its productive needs, it follows that it will not be able to sustain its growth spurt for very long. As Table 3 shows, imported inputs occupy an ever-greater proportion of all inputs consumed by Pakistan’s economy. As a result, Pakistan’s exports are also heavily dependent on imports[10], thus creating a situation where the goal of export promotion and import restriction may cancel each other out.

| Imported Inputs as a Percentage of Total Inputs | ||

| Sector | 2000 | 2022 |

| Coke, refined petroleum, and nuclear fuel | 33% | 44% |

| Chemicals and chemical products | 18% | 24% |

| Rubber and plastics | 23% | 31% |

| Machinery | 19% | 27% |

| Electrical and optical equipment | 33% | 45% |

| Transport equipment | 38% | 52% |

| Construction | 15% | 21% |

Table 3: Imported Inputs as a % of Total Intermediate Goods Source: Author’s calculations based on Pakistan’s Input-Output Tables

This gives birth to two critical questions: firstly, how can the Pakistani economy turn this tide?

Building an industrial base in any ‘late-developing economy’— Pakistan being no exception— may “not involve doing anything new from a global point of view”. Yet, it “poses a similar incentive problem because it is still a ‘new thing’ for the nation”.[11] This follows from the simple fact that to industrialize in a competitive world, a late-developing country must create sufficient rents for firms to justify the risk of starting new industries in that country and not somewhere else. “Such risk” implies that “those who are starting new industries in a late-developing country have to be provided with some form of entry barrier and the resulting rents”.[12] This has been the path of all ‘late-developing’ economies, including Germany, Japan, and Korea. It is also the central idea latent in the aspirations of the Indian state and its business owners.

Second, can the process of industrial policymaking be seen in isolation from the political economy that underpins it? The state is never an uncontested site. Its institutional prowess always produces winners and losers. Darron Acemoglu, a preeminent scholar on comparative development has convincingly demonstrated this through a host of empirical studies. But the underlying logic is simple to grasp. There are broadly speaking two fundamental institutions: economic institutions, which deal with the distribution of resources in a society versus political institutions, which pertain to the distribution of power. Acemoglu demonstrates that political institutions, that is the balance of power, dictate the trajectory of economic institutions: those in power at time t will redirect scarce resources towards their interests at time t + 1 and over time the economy will produce its winners and losers.

Any discussion of whether the state should intervene, which is separated from the question of who the prospective winners and losers will be, is then a purely scholastic question. It is clear who the losers are in the Pakistani case. But to understand what is wrong with Pakistan’s industrial policy one must only look around and ask: who are the winners?

The author is an Associate Professor of Economics at Bucknell University.

_____________

[1] https://www.thenews.com.pk/print/1131214-fauji-foods-plans-expansion

[2] Alice Amsden, The Role of Elites in Economic Development, 2014; Oxford University Press

[3] Ibid

[4] Ibid

[5] Dani Rodrik, “Industrial Policy: Don’t ask why, ask how”, Middle East Development Journal, 2008

[6] Priyanka Wandhe, “An Overview on Production Linked Incentive Scheme by the Government of India”, 2024,

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4693578

[7] Ibid

[8] Mubarak Ali, “Water Use Efficiency, Pakistan’s Fertilizer Sector Structure, Performance, Policies, and Impacts”: Pakistan Institute of Development Economics P & R October 2021

[9] Mushtaq Khan, “The Political Economy of Industrial Policy in Asia and Latin America”, Industrial Policy and Development. Oxford: Oxford University Press 2009

[10] Kaiser Bengali (2021) finds a correlation of 0.98.

[11] Ha Joon Chang, “Industrial Policy in Korea”, Cambridge Journal of Economics, 2006

[12] Ibid