Over the past few decades, Pakistan’s retail sector has seen a number of domestic brands penetrate the domestic commerce market. Many of these brands operate through the chain store retail model. These chain store businesses are an integral part of the formal retail sector in Pakistan and contribute significantly by providing employment and paying taxes. Yet, despite their critical role in the economy, only limited research is available on the breadth of the business networks of these brands and how they operate.

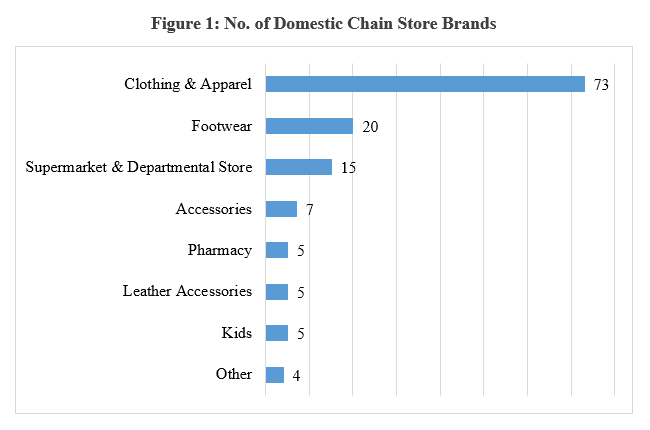

There are an estimated 134 domestic chain store brands in Pakistan. Out of the 134 estimated domestic chain store brands in Pakistan, 73 (54%) belong to the clothing & apparel segment, making it the largest segment in the chain store market. Furthermore, 20 (15%) belong to footwear, 15 (11%) belong to supermarket & departmental stores, 7 (5%) belong to accessories, 5 (4%) belong to the kids’, 5 (4%) belong to the leather accessories, 5 (4%) belong to the pharmacy segments, respectively.

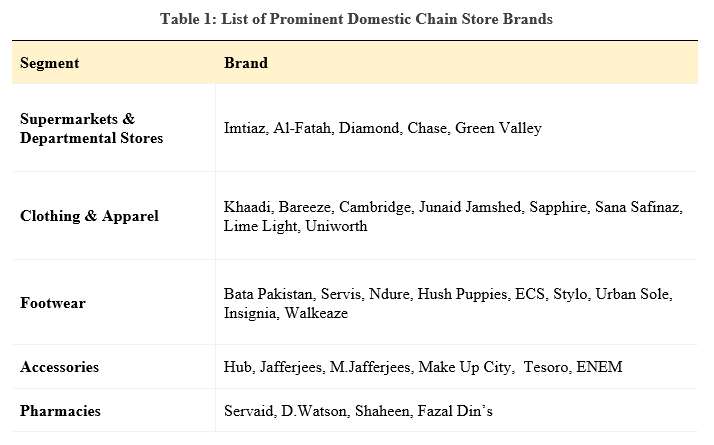

Table 1 lists prominent domestic chain store brands in each segment of the retail industry.

Given the dearth of structured and coherent information on the chain store businesses in Pakistan, it is first important to focus on mapping the domestic chain store sector itself. One important step in mapping the network of chain stores brands revolves around estimating the size and the geographical breadth of stores throughout the country.

Number of Chain Stores

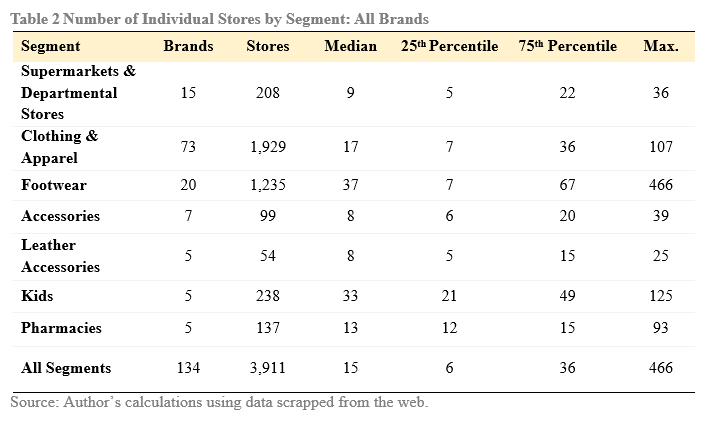

There is an estimated total of 3,911 chain stores in Pakistan. The estimated median number of stores for the 134 listed domestic chain store brands is 15 stores. Furthermore, the 25th percentile is approximately 6 stores, whereas the 75th percentile is approximately 36 stores. The smallest chain store brand in terms of its network has 1 store, whereas the largest chain store brand in terms of its network has 466 stores across Pakistan. Table 2 summarizes the median, 25th & 75th percentiles, and min and max for each of the segments within the chain store sector in Pakistan.

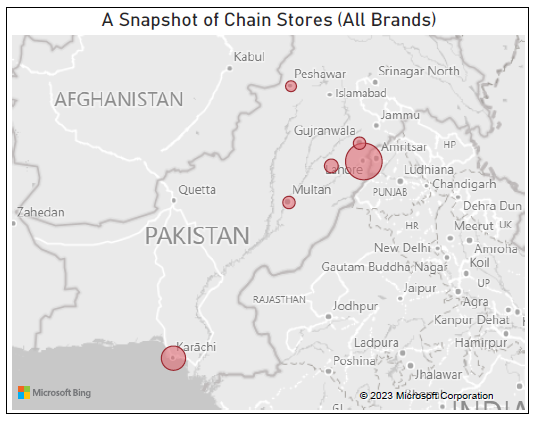

Chain Stores by Location

In terms of the location of individual chain stores across all brands, an estimated 50% of all individual stores are located in three metropolitan areas of Lahore, Karachi, and Islamabad/Rawalpindi. Lahore has 23% of all stores, followed by Karachi (13%), Islamabad/Rawalpindi (13%), Faisalabad (5%), Gujranwala (4%), Multan (4%), and Peshawar (3%). 34% of the remaining stores are spread across the rest of the country other in areas other than the aforementioned metropolitan areas.

Factors Impeding Growth

The last couple of decades have seen domestic chain stores establish a firm presence in the formal retail sector in Pakistan. However, there are certain points that have impeded and continue to impede the growth of the chain store sector in Pakistan.

Pakistani chain store brands despite their growing network do not have enough stores to cater to the population. The issue is further exacerbated by the high concentration of stores in three major metropolitan areas i.e. Karachi, Lahore, and Rawalpindi/Islamabad.

Regional Comparison: Supermarkets Chain Stores – Pakistan vs. India

Despite the growth in chain store brands and their national coverage. The chain stores segment in Pakistan still is in its early stages of development.

A key indicator of this is that Pakistan’s Top 5 supermarket chain stores brands have an average of 28 stores nationwide only. Whereas, Pakistan’s neighboring India’s Top 5 supermarket chain store brands have an average of 296 stores.

India population is about 6 times that of Pakistan. Deflating the averages above according to population, Pakistan’s Top 5 supermarket chain store brands should have at least 50 stores each (26 is the current average) to be on par with its neighboring India.

Furthermore, nearly all of the chain store businesses in Pakistan, even the ones with extensive store networks, are either sole proprietorships or family-owned businesses. In order to grow and contribute to the economy at a larger scale, these businesses need to professionalize and be willing to offer equity to investors and ideally list themselves on the stock exchange.

Professionalizing their businesses in this manner would also allow these businesses to grow outside Pakistan. This is important because despite its growth as a domestic sector, Pakistani chain store brands,

Pakistani Chain Store Brands in International Markets

Despite its growth as a domestic sector, Pakistani chain store brands, on the whole, have not been able to build their international profiles and penetrate the international markets.

- Pakistani Department Stores/Hypermarkets have not yet been able to penetrate the International markets.

A few clothing and apparel brands have established stores in international locations, but they still only cater to Pakistani and South Asian Diasporas and have ethnic product ranges.

on the whole, have not been able to build their international profiles and penetrate the international markets. Only a few clothing & apparel brands have established some presence in international markets with significant South Asian Diasporas. Yet, even these market penetrations are at their nascent stages.

The chain store sector in Pakistan is a cornerstone of the formal retail sector in the country. However, the businesses in the sector need to expand both locally and internationally. This is only possible by improving quality standards and by letting go the ‘seth’ culture that permeates through the ownership and management structures of these businesses.

The author is a Research Fellow at the Pakistan Institute of Development Economics (PIDE), Islamabad.