The real estate market is an arrangement where the buying, selling, renting, and leasing of developed, underdeveloped, and undeveloped real estate properties occurs. It is a vital component of the broader economy that includes a wide range of activities related to commercial, residential, industrial, and other properties (PACRA, 2022). The real estate sector is considered one of the key sectors in Pakistan because of its contribution to the GDP.[1] Due to backward linkages to the construction-related industries, this sector has also been considered the driver of growth for the economy.

In Pakistan, however, as noted by Haque (2015, 2020), excessive zoning has stifled construction of the high value-added side of real estate and forced people to go into green field development which is full of malpractices and excessive delays.

_____________

[1] Ullah and Najib (2022) have estimated that the real estate assets in Pakistan account for USD 300 to 400 billion.

_____________

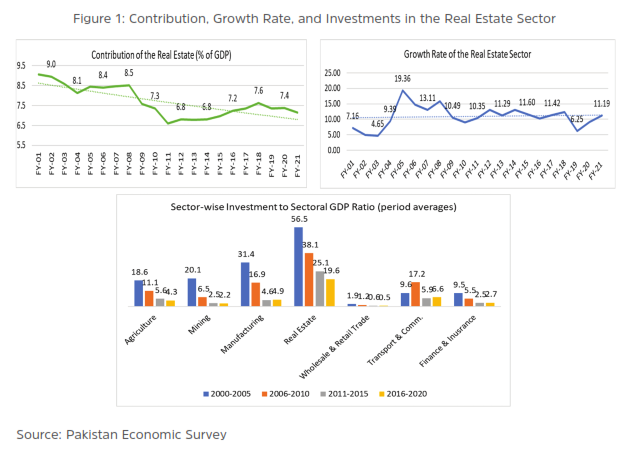

Although this sector has seen a huge inflow of investment, its growth is almost stagnant with a declining contribution to the GDP (see Figure 1). This is because of the peculiar way in which this sector is regulated to create a slowly expanding sprawl that locks in people’s savings for decades.

Real estate is a serious contributor to growth in many countries. In fact, it is regarded as a leading indicator in most economics. Why is real estate not contributing to GDP growth even though inflows into the sector anecdotally remain high?

Yet the real estate market is innovating in its own domain in keeping with the regulatory framework offered to One such innovation is the files – an option on a potential plot – in a development that is happening,

This brief aims to explore the connection between the prevalence of the file culture and the sluggish growth of the real estate market.[2]

- Genesis of File Culture

The rapid urbanization and population growth have resulted in a high demand for urban real estate. The bureaucracy that runs cities in the absence of local government has developed zoning rules that restrict mix-use and high-rise development in city centers. Ultimately, cities started to grow horizontally instead of vertically (Haque, 2015).

| Box 1: Cooperative Vs. Private Housing Societies in Islamabad Cooperative Housing Societies

Private Housing Societies

|

________________

[2] We call is “Plotistan” in PIDE

________________

These horizontal expansions of cities are carried out by allowing the development of housing societies because the development authorities anticipate that it is a cost-efficient and swift way to cater to the increasing demand for real estate in cities.[3] The prime objective of these housing societies is to provide housing options to people along with all the basic facilities. The cities saw the emergence of cooperative housing societies followed by the mushroom growth of private housing societies.

| Box 2: Cooperative Housing Societies The foundation of cooperative societies in Pakistan is rooted back to the Cooperative Societies Act of 1912. The idea behind cooperative housing societies was to provide affordable housing to less affording people of India. Later, under the Government of India Act of 1919, the authority to make laws regarding the administration and development of cooperative societies was handed over to provinces. After that, the Cooperative Societies Act was passed in 1925 and all the cooperative societies in Pakistan are regulated under this act. Cooperative Housing Societies in Pakistan In 1949, the Karachi Cooperative Housing Societies Union was founded. The government leased more than 1,200 acres of land to the union for the township development. In Punjab, cooperative housing societies began to be established in the 1970s. However, in the mid-1990s, a corruption scandal surfaced in which housing cooperatives had practiced fraud with thousands of people who had invested in cooperative housing societies. The Punjab government compensated the affectees and imposed a ban on the registration of cooperative housing societies in 1997, which was later uplifted. Cooperative housing societies in Pakistan are developed under the township model. Large pieces of land are provided by the government to the cooperative housing societies. Rules and Regulations of Cooperative Housing Societies Cooperative housing societies in each province operate according to the by-laws of the cooperative housing society made by the provincial cooperative societies’ authority. These authorities regulate different cooperative societies in their province under the Cooperative Societies Acts, which originated from the Cooperative Societies Act 1925. Cooperative housing societies are registered with the registrar of cooperative societies in each province. Key sections in this regard are:

According to Section 68, cooperative societies, including cooperative housing societies cannot be regulated by the Securities and Exchange Commission of Pakistan (SECP). They are regulated by the registrar of cooperative societies. Do we need Cooperative Housing Societies or not? The phenomenal growth of cooperative housing societies that crowd out the private sector, for instance, there are more than 254 cooperative housing societies in Punjab, poses serious considerations about the need for cooperative housing societies. Besides frequent fraud incidents and mismanagement also pointed towards the increase of the role of private developers in the market.

|

________________

[3] Mehmood (2022) provides a detailed historical account of the development of housing societies in the real estate sector of Pakistan.

_______________

Initially, the modus operandi of these housing societies was to offer plots to their members or individuals so that they could construct and develop these pieces of land. However, the increasing real estate demand and sluggish development of residential sectors led to an increase in plot prices in those housing societies. This phenomenon invites speculative investors, therefore, demand for housing societies further increased.[4] The housing societies began offering plot titles instead of plot possessions to initiate more housing projects without huge capital investments.

| Box 3: Illegalities in Housing Societies The private housing societies and their legality have recently gained much traction in popular media and policy circles. CDA estimates that of 204 housing societies in Islamabad, 140 are illegal. Our study of the status of other 64 “Authorized” societies suggests that only 22 housing societies have the required documents. This puts legal societies at 10 percent of the total. A special audit report by the Accountant General of Pakistan (2017) presents an even more dismal picture. It suggests that over 90 percent of the land (1.26 million Kanals) in Zone 2, 4, and 5, is not under the purview of CDA as societies with NOC make up less than 7% of the area. Most government departments, both civilian and military, are in the business of building housing societies. Source: Hasan et al. (2021) |

According to the PIDE Sludge Audit, the development of housing societies and the process of handing over possession takes approximately 20 years. Consequently, the actual demand for housing units remains unmet. Real estate developers start the practice of selling promises or pledges to buyers that a plot of a specific size will be provided in the proposed housing society provided you pay the price upfront – this practice is commonly known as “file trading.” Now the predominate transactions involve the purchase of the right to purchase a plot (files) even before the developers acquired the proposed land.

________________

[4] In the case of Pakistan, it is commonly perceived that real estate investment in the form of buying a piece of land or buying a house comparatively yields the highest returns. Qasim and Aslam (forthcoming) show that investment in stock offers the highest average annual returns. The real annual average return from shareholdings is 8.6 percent against 8.1 percent from residential real estate from 2011 to 2021. Fraz (2022) has also shown that the nominal rate of return from real estate from 2012 to 2015 varies from 25 to 14 percent, however, stock investment generated higher returns.

_______________