Don’t Fall in Love with Parity: Understanding Exchange Rate Depreciation

Key Takeaways from Global Research

- Exchange rate is like temperature in a human body: it merely reflects underlying weaknesses. Like the human body artificially holding the temperature down for long periods without addressing the causes is likely to lead to grievous consequences.

- There is no such thing as an active devaluation policy for boosting exports.

- Holding the exchange rate at an artificially appreciated rate is only possible through reserve loss. These losses cannot be incurred over the long run as reserves are finite and market participants know that reserves can be attacked to their advantage.

- Bolstering the exchange rate through exchange and import controls serves only to disrupt supply chains and eventually weaken the domestic economy. At best it is a short-run painful solution.

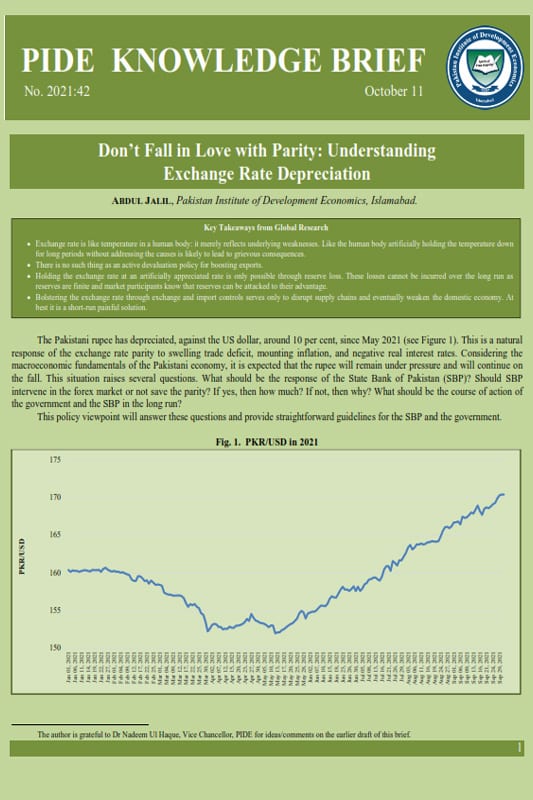

The Pakistani rupee has depreciated, against the US dollar, around 10 per cent, since May 2021 (see Figure 1). This is a natural response of the exchange rate parity to swelling trade deficit, mounting inflation, and negative real interest rates. Considering the macroeconomic fundamentals of the Pakistani economy, it is expected that the rupee will remain under pressure and will continue on the fall. This situation raises several questions. What should be the response of the State Bank of Pakistan (SBP)? Should SBP intervene in the forex market or not save the parity? If yes, then how much? If not, then why? What should be the course of action of the government and the SBP in the long run?

This policy viewpoint will answer these questions and provide straightforward guidelines for the SBP and the government.  ___________________________________

___________________________________

The author is grateful to Dr. Nadeem Ul Haque, Vice Chancellor, PIDE for ideas/comments on the earlier draft of this brief.

SHOULD SBP CONTINUOUSLY SAVE THE EXCHANGE RATE PARITY THROUGH FOREIGN EXCHANGE INTERVENTION?

The answer is NO.

It is being argued that the exchange rate is continuously depreciating despite having a handsome amount of foreign exchange reserves. So, this is ‘against the fundamentals of economics that the foreign exchange reserves are increasing and, on the other hand, the rupee is depreciating. So, SBP should manage the pressure on the exchange rate through the intervention in the foreign exchange market (see Box 1).

| Box: 1: Exchange Rate Pressure: Managed or not Managed When there is a mismatch between the demand of the foreign currency (dollars in our case), and the supply of the foreign currency than the home currency (Pak rupee in our case) remain under pressure to depreciate or appreciate. In this case, the central bank, SBP in our case, may intervene in the foreign exchange market through the selling or buying of the foreign currency to manage the pressure. The difference between the actual nominal exchange rate and the equilibrium exchange rate is called the unmanaged portion of the pressure. If the actual exchange rate is equal to the equilibrium exchange rate, then SBP is not managing the exchange rate. If the actual exchange rate is overvalued when the demand of the dollar is higher than the supply of the dollar, then the pressure is fully managed by the SBP(see Jalil 2021 and Rao 2019 for the details and calculations of exchange market pressures and management). |

We argue that the SBP should not intervene in the forex market. It is very clear that the amount of foreign exchange reserve is not in the safe zone. As per the SBP data, Pakistan’s liquid foreign exchange reserves are around 26.1 billion USD (19.2 billion USD SBP reserve and 6.8 billion USD commercial bank reserve). It is also important to mention that we availed several debt reliefs and additional finances during COVID. If we net off all these finances, roughly, the foreign exchange reserves level will be around 20 billion USD.

On the other hand, the import bill is around 6 billion USD per month and growing in the backdrop of post-COVID recovery and increasing international commodity prices. According to these numbers, the foreign exchange reserves provide only the coverage of 3.0 to 3.5 months imports coverage. So, the reserves are not in the safe zone. If SBP intervenes in the foreign exchange market by selling the dollars, then foreign exchange reserves’ loss is very obvious. That’s why, keeping in view the pressure on the external sector in the future and the level of foreign exchange reserve, it is not advisable, in any case, that SBP should intervene continuously.

If SBP intervenes continuously, the loss of foreign exchange reserves will lead to balance of payment (BOP) crises. The obvious outcome is to approach to International Monetary Fund (IMF) to manage the BOP crises. The heart of the IMF loan-led policy is ‘stabilisation’ and ‘the market-based exchange rate.’ Consequently, the SBP intervention in the forex market will lead to loss of reserve, BOP crises, depreciation of the currency, and compromise on the GDP growth.

THEN WHAT ARE THE OTHER OPTIONS?

The SBP has other options in this challenging situation that are not being utilised. We think that SBP should seriously think on these lines.

Publicly Announced Interventions in the Foreign Exchange Market

The important thing is that the SBP should intervene in the foreign exchange market to curb the extra volatility and the artificial demand in the foreign exchange market. The extra volatility and the artificial demand are creating uncertainty in the foreign exchange market. Indeed, this situation is prone to speculative attacks and untargeted bidding (see Box 2). First and foremost, the task of the SBP should tackle this situation to save the market from speculative attacks.

| Box 2: Untargeted Bidding in the Foreign Exchange Market The untargeted bidding phenomenon often happens in the forex market when the traders feel uncertainty about the speed of the movement of exchange rate parity. It means that when a foreign exchange dealer just takes the ask/bid rate from the other dealer without committing the deal. This, just asking the rate, generates expectations about excess demand and excess supply in the market. Ultimately this creates the artificial demand and supply of the foreign currency in the forex market. It is also important to mention that the untargeted bidding can generate a very irrational number of order flow, based on the number of buyers and sellers, while the amount of buying and selling do not indicate the same trend. |

One of the most important tools is the publicly announced intervention. The SBP should adequately communicate about the size and the sign of the foreign exchange intervention. When an artificial buyer will have information that the SBP will intervene to save the parity, this will discourage his/her intention of buying or dollarisation. So, the publicly announced intervention may curb the unnecessary artificial demand of the dollars and the speculative attacks.

Recently, Patel and Cavllino (2019) surveyed several central banks and concluded that the publicly announced intervention significantly strengthens the signalling effect of the market. This is not new evidence or advice. Sarno and Taylor (2001) is a valuable read in this regard.

Importantly, this is growing practice among the central banks that they intervene publicly and remain transparent in the forex market. However, this phenomenon is more common in Latin American economies than in Asian economies (see Patel and Cavllino, 2019). Patel and Cavllino (2019) also argue that transparency and publicly announced intervention have advantages. It sets a signal from the central bank that what is going to happen in the future. Similarly, it enhances the credibility of the central bank. A credible commitment regarding the intervention or no intervention reinforces the signalling effect.

Should Focus on the Market Intelligence

However, there is no question that market intelligence is key to success. The knowledge about the intensity and the persistence of the exchange rate pressure may help determine the level of the foreign exchange intervention for anchoring the volatility of the exchange rate. If the pressure is persistent and due to structural issues, then it is better not to intervene. Otherwise, the forex traders will trade in the opposite direction of the central bank, and the central bank may deplete reserves without much impact on the volatility and the parity. Both announced interventions and secret interventions don’t work in this case.

Proper Communication to Curb any Conspiracy Theory

The SBP should get accurate information about the inflows and outflows of the foreign exchange and then correctly communicate to the stakeholders to curb any conspiracy theory. For example, recently, there has been a rumour that the dollar is being transacted on Afghanistan’s borders. The volume of these transactions is not precisely known. It may be possible that the actual volume is very low. But the rumours of ‘huge transactions’ are creating uncertainty and artificial demand. Unfortunately, the government is also hiding herself and the structural issues behind these rumours. This is more dangerous than the actual situation. Therefore, SBP and the government should adequately investigate the number and volume of the transactions. Then it should be properly communicated to the relevant stakeholders. This is also true in all other cases where the artificial demand and supply of dollars may create uncertainties. This act of SBP and the government will reinforce the credibility of the central bank. Indeed, the action of any credible central bank matter a lot to reduce speculative attacks.

Communication about the Equilibrium Exchange Rate

Jalil (2021) clearly shows that the undervalued/undervalued exchange rate has a positive/negative impact on economic activities. Therefore, SBP should continuously monitor the equilibrium value of the exchange rate and then properly communicate to the stakeholder. This will further signal to the stakeholder about the direction and the extent of the movement of the exchange rate and the intervention of the SBP into the foreign exchange market. This may also enhance the credibility of the SBP and may curb the extra artificial pressure on the home currency.

Very Calculated Tightening of Monetary Policy

The current monetary policy statement (MPS) of the SBP increases the policy rate to indicate that the SBP has changed its stance in the backdrop of rising inflation due to the increased demand. This is further linked with the revival of economic growth and the recovery from COVID-related recession. Partially, it is true that the prices have been increased due to the rise in demand. But there is another version that the supply chain is disrupted due to the Covid. If this is the case, then the monetary policy’s tightening will not help curb the cost-push inflation pressure. The rising interest rate will hit both sides, that is, slow down the revival of the growth and increase the cost-push inflation. Surely, the rising inflation will hit the poor of the society and competitiveness as well. So, the SBP should track the actual reasons and size of the demand and supply-side pressures on inflation and act accordingly in the context of tightening the monetary policy.

LONG RUN STRATEGY

Don’t Fall in Love with Parity

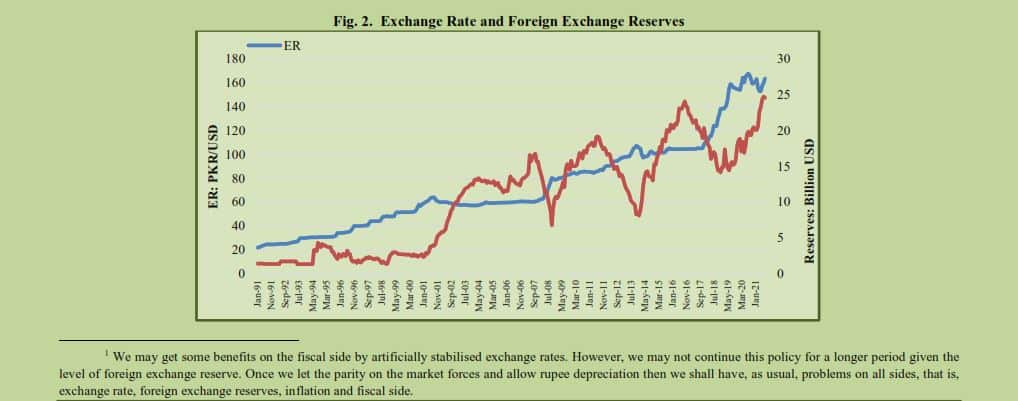

It is highly recommended that the exchange rate parity should move with the market forces. Historically, whenever the SBP intervened in the forex market to stabilise the exchange rate against the market forces then after some period the loss of foreign exchange reserves was the obvious outcome (see Figure 2) and the BOP crises.[1] This led to the IMF program. Consequently, we had to over-adjust the rupee to follow the IMF program. This led to both depreciation and the loss of foreign exchange reserves. Therefore, the SBP should not repeat the old mistake. If SBP and government claim that this is a new regime and the ‘parity can move in both ways’, then the SBP and government should not panic. They should be bold enough to wait for the natural movement of the exchange rate. They should let the rupee on the market forces with anchoring the artificial pressure and artificial uncertainties.

Clear-cut Structural Reforms to Ease the Pressure on the External Sector

If a country has chronic issues in the BOP, then the home currency cannot be stabilised for a more extended period. Therefore, Pakistan should concentrate on the long-term strategy to recover the BOP issues. Merely, depreciation will not correct the current account deficit (CAD) or trade deficit issues. It may partially, keeping rigidities given imports, reduce the imports. But the exports cannot be flourished with the depreciation only. Because we have several limitations with the exports on the front of narrow base, regulations, governance and international diplomacy. It is very obvious that the regulations have to be improved, simplified and streamlined. Without improving the external sector, the issue in the currency would not be resolved.

Accumulate Foreign Exchange Reserves

As mentioned earlier, the foreign exchange reserves of Pakistan are not in a safe zone according to reserves adequacy ratios. Therefore, the SBP should accumulate foreign exchange reserves. On the one hand, aforesaid should intervene in the foreign exchange market by selling the dollars to save or reverse the parity. On the other hand, the SBP should purchase the dollars from the forex market whenever possible. Last year, there was an excellent chance to buy the dollars from the market. However, the SBP let the PKR appreciate from 168 per USD to 151 per USD by announcing that the parity will move both sides. The SBP could purchase a heavy amount of dollars through purchasing and could maintain the rupee undervalue.[2] This would not be a unique case. The SBP purchased a heavy amount of dollars from the market in the early 2000s (see Hussain and Jalil, 2006).

Don’t Put Exchange Controls

The SBP should not strengthen the local currency through foreign exchange control and import controls. Indeed, this act will serve only to disrupt supply chains and eventually weaken the domestic economy. At best, it is a painful short-run solution. It is well documented in the literature that foreign exchange restrictions spawn the parallel currency markets and the parallel exchange rate.[3] The premium between the official rate and the kerb rate reflects the sign of devaluation/depreciation. Therefore, ultimately, the currency has to be depreciated along with a high cost. We have witnessed the kerb exchange market and the dual exchange rate in Pakistan during the 1980s and 1990s.

CONCLUDING AND WAY FORWARD

This note discussed several options for the SBP and the government in the backdrop of currency depreciation and uncertainty in the forex market. We suggest that SBP should:

- Public information about the size and direction of the foreign exchange interventions in the foreign exchange market.

- Properly communicate with the stakeholders about the transactions of the dollars.

- Educate the stakeholders about the market value of the exchange rate.

- Move towards the tightening of monetary policy in a very calculated way.

We believe that these steps will curb artificial volatility and artificial demand in the short run. Secondly, the intervention in the forex market on a long-term basis is not advisable in any case. The cost is huge as we have experienced in the past. Third, the structural reforms are indispensable for the correction of the chronic issue in the BOP. We want to clear that we are not against the intervention in the forex market to curb the extra uncertainty in the forex market, but there must be a tolerance level. More clearly, this note is to inform the fear of nominal exchange rate fluctuations and especially of future depreciation. We believe that the debate on this issue will lead to a better monetary and exchange rate policy.

REFERENCES

Hussain, F. & Jalil, A. (2006). Effectiveness of foreign exchange intervention: Evidence from Pakistan. State Bank of Pakistan, Research Department. (SBP Working Paper Series 14).

Jalil, A. (2021). Exchange rate policy must seek undervaluation! Pakistan Institute of Development Economics (PIDE), Islamabad. (Knowledge Brief 1).

Pate, N. & Cavllino (2019). FX intervention: Goals, strategies and tactics. BIS Papers chapters. In Bank for International Settlements (ed.), Reserve management and FX intervention, volume 104, pages 25-44, Bank for International Settlements.

Rao, N. H. (2019). Effectiveness of monetary policy in controlling exchange market pressures: Case of Pakistan. Department of Economics and Finance, Pakistan Institute of Development Economics (PIDE). (MPhil Thesis).

Sarno, L. & Taylor, M. P. (2001). Official intervention in the foreign exchange market: Is it effective and, if so, how does it work? Journal of Economic Literature, 39, 839–868.

___________________________________________

[2] See Jalil (2021) on the policy of undervaluation.

[3] It is known as Kerb rate in the history of Pakistan international finance.