Key Takeaways

|

1. What is Net Metering?

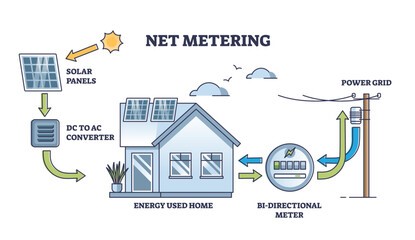

Source: https://www.istockphoto.com/vector/net-metering-system-for-renewable-electricity-generation-outline-diagram-gm2076455285-564930688

Distributed Generation (DG) improves energy security. Its appropriate technical design and specification can be crucial in providing auxiliary services for grid support (SAARC, 2021). Net metering (NM) is a policy tool that promotes distributed renewable energy generation by incentivizing behind-the-meter DG deployment to meet policy objectives (clean energy, resource diversity, economic development, and resilience) and customer expectations for energy choices and savings (National Academy of Sciences, 2023). Many technologies qualify for NM, e.g., solar photovoltaic (PV), wind, small hydro, biomass, biogas, geothermal, etc. Yet, excluding solar, others depend on site-specific resources and are not widely used.

Under NM, a consumer (also known as a prosumer) installs an on-site renewable energy (RE) power plant (e.g., rooftop solar). It allows consumers to reduce reliance on grid electricity, makes solar investments financially viable, and alleviates pressure on peak demand and transmission losses. It empowers customers, helps balance rising electricity bills, and reduces greenhouse gas emissions by increasing the grid’s share of renewable energy (RE) sources.

The consumer remains connected to the grid and can supply surplus energy to the national grid. These surplus units are recorded and later subtracted from the units consumed from the grid. This incentive scheme ensures consumers benefit from electricity generated by their system, whether used personally or fed into the grid.

Various incentive schemes (other than NM) are in practice globally (Box 1). These schemes have led to the widespread adoption of RE, benefiting the grid with a cost-effective clean energy supply.

| Box 1. Incentive Schemes to Promote Rooftop Solar Net metering (NM) allows consumers (prosumers) to offset their electricity consumption with the energy they generate. It credits for any surplus energy at the retail rate. It requires the installation of a bidirectional meter that runs backward when exporting electricity, offsetting the amount of electricity used against the generated amount. NM does not typically involve a monetary exchange. Instead, the credits accumulated through NM are stored and utilized when drawing electricity from the grid when solar energy is not generated. By definition, NM credits can be rolled over monthly and are usually a one-on-one exchange; solar panels’ kilowatt-hours (kWh) are worth the same as a grid-produced kWh. This simplifies the energy bill as the prosumer is billed for net energy use (energy consumption minus energy production). Net billing (NB) involves the monetary exchange of energy. Consumers can offset their power consumption with self-generated energy. However, the credits earned through NB are based on the wholesale rate of electricity, which is lower than the retail rate credited under NM. This results in reduced financial benefits compared to NM. Prosumers can sell their excess energy to the utility at wholesale rates, similar to how large-scale solar projects operate. Gross metering (or Feed-in-Tariff (FIT)) represents a more distinct approach, where all generated energy is fed directly into the grid and is compensated at a predetermined FIT. Meanwhile, all consumed energy is purchased from the grid at retail rates, completely decoupling generation from consumption. Time-of-Use (TOU) where exports and/or imports are priced based on time of day and seasons. The pricing structure is assessed, communicated to prosumers, and revised from time to time, based on changes in market and grid conditions. Exports and imports of power from a prosumer are valued in 15 minute/hourly time windows and the final energy bill is prepared over the billing period (normally monthly). TOU pricing helps in incentivizing prosumers to export more during peak hours and consume more during off peak hours. This helps in balancing energy systems and reduces requirements for additional network capacity. A well-designed TOU pricing may support energy storage investments. Virtual Net metering or Net billing involves subscribing to a local community solar farm and sharing the net metering/ billing credits generated by the solar farm among all subscribers. Source: https://freyrenergy.com/net-metering-vs-gross-metering-vs-net-billing-is-one-better-than-the-others/ |

2. Impediments to Net Metering

NM is also faced with certain challenges which require a well-thought strategy[1].

Intermittency: The unpredictability of energy production ̶ renewable sources like solar and wind rely on external factors such as weather and time of day. Sunshine and wind speed are inconsistent due to changing seasons and daily weather patterns. The variability of solar energy production can result in periods of overproduction or underproduction. For example, a solar panel may generate more energy on a sunny summer afternoon, but production decreases significantly during a foggy or rainy day. This creates challenges in aligning energy supply with demand and can complicate energy transfer to the grid, impacting reliability and stability.

Grid Stability: The grid infrastructure is typically designed for one-way electricity flow. NM introduces a reverse power flow, causing operational problems such as voltage spikes—damaging equipment, and potentially destabilizing the grid. Grid management practices need to be overhauled to accommodate this bidirectional energy flow. Additionally, having too many solar PV systems in a specific area could overwhelm the local grid, leading to potential grid stability issues due to excess energy.

Grid operators must balance energy supply and demand to keep the grid stable. However, managing this balance becomes more complex with the added variable of homes and businesses supplying back energy at different times and quantities. Therefore, grid management practices need a significant overhaul to effectively accommodate this bi-directional energy flow, which is challenging for financially weak utilities.

Furthermore, single-phase NM and three-phase NM share many challenges, such as generation unpredictability, power quality, and voltage regulation. However, single-phase NM presents an additional challenge: it can lead to phase imbalances if the connections are not evenly distributed across different phases (GIZ, 2021).

Fairness: Ensuring fair compensation for investment in RE installations is quite complex. The cost of electricity is a multifaceted equation influenced by factors such as demand, fuel pricing, and the time of day, making it challenging to determine a fair price for electricity generated from RE sources and injected into the grid.

Moreover, the implications of this issue are not limited to prosumers but can potentially affect all grid consumers—those who do not have solar PV systems. These customers may face higher electricity rates to cover the increased grid costs caused by the shifting of NM customers. A further argument is that the NM participants may need to contribute their fair share to grid maintenance or system costs. This debate raises questions about configuring compensation for NM participants and other electricity consumers.

NM has not been viewed positively by utilities. It is perceived as resulting in loss of customers (revenue), adding costs to manage infirm power generation, and leaving utilities with committed fixed costs to be allocated to non-NM consumers. Utilities have developed and adopted FIT schemes to treat DG as simply a generation source. However, this is not attractive to many customers (SAARC, 2021).

3. Net Metering Global Perspective

The information in this sub-section is gathered from multiple sources, including SAARC (2021), GIZ (2017, 2024), Ramalho et al. (2017), Abdin and Noussan (2018), Klein (2024), Karthik (2023), (Uibeleisen & Groneberg, 2024), (Yuen, 2024), and various web sources mentioned as needed.

The global solar energy market’s installed base is expected to grow from 1.84 million GWh in 2024 to 5.08 million GWh by 2029[2]. Favorable government policies and decreasing solar PV system costs are expected to boost the global solar energy market.

Countries worldwide have implemented NM programs. Its effectiveness, however, depends on the regulatory design and its effectiveness, the institutional capacity of electricity distribution companies, and a supportive market environment. Initially, utilities opposed NM due to revenue concerns, but government RE targets led to implementation. Later, utilities recognized its benefits – its competitive price and support for the grid’s performance goals.

NM was first initiated in 1979 in the State of Massachusetts, United States of America (USA). The policy gained popularity in the 1980s in the USA[3], followed by Japan in the 1990s[4], before being implemented worldwide to promote consumer ownership of electricity generation. Germany introduced the first FIT scheme in the world[5]. Australians are among the world leaders in solar power adoption[6].

Box 2. NM and RE Capacity Expansion

significant cost reductions in PV installations. |

NM Capacity Cap

- Normally, 100% of the sanctioned load is permitted as permissible NM capacity for on-site RE, e.g., in India, Bangladesh, and Saudi Arab.

- Net metering policies usually start with limited permissions for DG vis-à-vis the grid capacity. They typically restrict cumulative renewable energy capacity on a distribution feeder to 15% of feeder capacity or peak sanctioned load. However, these limits have evolved, and now, the limit has been raised to 100% of the grid’s peak capacity with minimal investment in transformer load management systems[7].

- In India, up to 15-75% of distribution transformer load capacity allowed across States. Grid integration studies indicate extension up to 100% DG capacity without posing significant challenges.

Grid Challenges

- In Europe, most countries use a merit order priority system for deploying renewables. Germany has strict rules – grid operators can request a reduction in renewable capacity but with a valid explanation. If revenue loss due to grid congestion is more than 1% of annual revenues, affected operators are fully compensated.

- During 2004-2009, Italy experienced growth in solar and wind projects, causing grid congestion due to the mismatch between generation and load centers. Italy implemented Dynamic Line Rating (DLR) systems to manage real-time grid capacity variations, reducing curtailment and improving efficiency.

- On the contrary, with its uneven transmission and distribution infrastructure, Vietnam finds accommodating the new solar and wind projects onto the grid challenging after 2020.

- Grid stability concerns, especially in dense populations, have been managed by integrating NM technologies with better equipment, grid codes, and utility controls.

- In Germany, excessive rooftop solar generation during peak sunlight caused grid frequency issues. Balancing supply and demand in real-time became challenging. Consequently, Germany updated its grid codes, imposing stricter requirements on new solar installations[8].

Automation

- Countries like India and Germany are increasingly deploying automated metering infrastructure (AMI) to improve monitoring and oversight.

- A new law passed in Germany requires all consumers using over 6,000 kWh annually and RE operators with over 7kW capacity to install smart meters by 2025[9].

Compensation Schemes

- NM compensation starts with retail tariff, FIT, generation-based incentives, and the carryover of credits allowed for one or more years. Over time, it has been revised and replaced with new schemes and incentives.

- Moreover, incentives/ compensation vary across States, utilities, or sectors in several countries, e.g., India, Australia, Germany, Italy, and the USA.

- In Japan, new FIT varies with system size and type, offering higher rates to residential rooftop solar PV with a capacity lower than 10kW.

- Germany introduced the first FIT scheme in the world. However, the compensation for PV for new power plants has decreased by around 85-90% (from a fixed tariff of 45 ct/kWh in 2005 to 5-6 ct/kWh in 2020).

- Furthermore, new schemes are introduced but not at the cost of old customers.

- In the USA, incentive schemes vary across States and utility companies—some states compensate each kWh at the full retail rate, while the majority offer a reduced solar buyback tariff[10]. Some States (e.g., Arizona, California, North Carolina, and Arkansas) have adjusted their net metering programs due to concerns about cost shifts for non-solar customers[11].

Box 3. Case of California Net Metering (NM) 3.0 vs Net Metering (NM) 2.0

Source: https://thecleanenergyalliance.org/clean-energy-alliance-explains-nem-2-0-vs-nem-3-0/#:~:text=The%20most%20notable%20difference%20between,3.0%20will%20have%20no%20impact. |

Implementing incentive programs like NM has further accelerated the global adoption of renewable energy. Integrating solar power with energy storage systems is expected to generate new market opportunities.

4. Net Metering in Pakistan

4.1. Current status of Solar PV in Pakistan

Pakistan, with its abundant solar irradiance, is poised to harness the power of the sun. With an average of nine and a half hours of sunlight daily, the potential of distributed solar PV to meet a significant portion of Pakistan’s electricity demand is promising. This is particularly beneficial for areas with high losses, unreliable, or limited grid supply.

In line with its 2030 emission reduction plan, Pakistan aims to reduce GHG emissions by 50% through an energy transition – directing approximately 60% of its energy mix towards RE. Solar PV can be a key player in securing Pakistan’s energy future by reducing reliance on imported fuels, mitigating power generation insufficiencies, and curbing high transmission and distribution losses. The Carbon Border Adjustment Mechanism (CBAM) by the European Union further reinforces this path, compelling Pakistan’s export industry to shift to RE to remain competitive in the global market by 2030.

Due to rising electricity costs, industries and commercial organizations are turning to captive solar solutions[12]. Likewise, domestic rooftop PV panel installations are increasing in large urban areas. NM regulations were enacted for projects under 1 MW in September 2015 to incentivize DG. Apart from some smaller installations, the development of solar power plants started in Pakistan with introducing the Upfront tariff for solar PV plants in 2015.

Table 1. Solar-based Electricity Generation in Pakistan as of June 30, 2023

| Solar PV Plant | Capacity (MW) | Dependable Capacity (MW) | Electricity Generated (GWh) | Last Determined Tariff (PKR/kWh) | License Period (Years) |

| Quaid-e-Azam Solar Power Limited | 100 | 52 | 160.47 | 31.23 | 25 |

| Crest Energy Private Limited | 100 | 100 | 169.83 | 49.14 | 30 |

| Best Green Energy Pakistan Limited | 100 | 100 | 166.17 | 48.80 | 25 |

| Apollo Solar Development Pakistan Limited | 100 | 100 | 165.83 | 46.29 | 25 |

| AJ Power | 12 | — | 18.35 | 29.40 | 26 |

| Harappa Solar | 18 | 18 | 31.07 | 29.68 | |

| Atlas Solar (formerly Zhenfa Pakistan New Energy) | 100 | 50 | 197.12 | 14.208 | 26 |

| Net Metering | 1055 | 1091.87 | 22.9 | 7 |

Source: NEPRA Licensing and Tariff Determinations

- In FY2023, six solar power plants generated electricity for the grid. As of June 30, 2023, the total grid-based installed capacity is 530MW (Table 1).

- All these plants are under a 25 to 30-year long-term agreement. In contrast, the NM regulations in Pakistan allow a 7-year agreement between the consumer and DISCO and do not ensure grid access.

- The upfront tariff for all these plants (except for Atlas Solar) is much higher than the NM tariff (Table 1).

- As per NEPRA tariff projections for FY2025, the projected power purchase price (PPP) for solar IPPs is PKR 37.18/ kWh, much higher than the currently allowed NM export tariff of PKR 22.9 /kWh and the projected average PPP of PKR 27 kWh.

4.2. Net Metering Regulation

Pakistan introduced the NM policy in 2006 (under the Policy for Development of Renewable Energy for Power Generation, 2006). It followed up with regulatory guidelines on September 01, 2015 (National Electric Power Regulatory Authority (NEPRA) Distributed Generation and Net Metering Regulations, 2015, notified via S.R.O. 892(1)1/2015), amended in 2017, 2018, 2020, and 2022 to promote power generation from distributed renewable energy installations.

NEPRA regulations allow distribution companies (DISCOs) to purchase excess units of electricity consumers (prosumers) produce and net them off against the units consumed from the grid. The potential market for NM is limited to three-phase consumers (TOU meters), which account for roughly 4% of all grid-connected electricity customers in the country.

NEPRA’s regulations require electricity units to be netted at off-peak rates, regardless of when the consumer supplies them. DISCOs will use off-peak time units and rates to net the electricity bill. Per regulations, the DISCO’s responsibility is to maintain phase balance in the secondary circuit of the distribution line to prevent load imbalance. The DG shall operate and inject power when the network is within the prescribed parameters.

- One of the flaws in regulation and its implementation is that approvals/ licenses are acquired after the installation at the premises.

- Even for smaller capacity installations, prior approval from the electricity inspector should have been compulsory to prevent any misuse or limit breach.

- Regulations do not prescribe a mechanism for the existing NM consumers to transition to a newer NM regime.

Box 4. Net Metering (NM) Regulation 2015 – Salient Features

|

4.3. Status of Net Metering in Pakistan

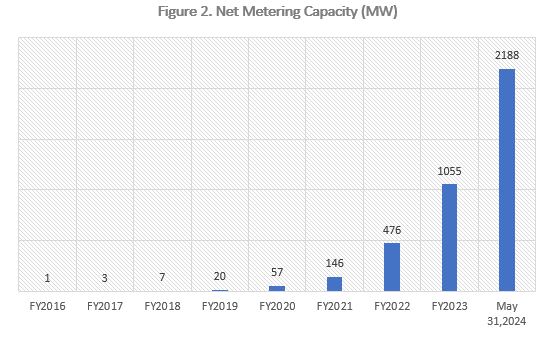

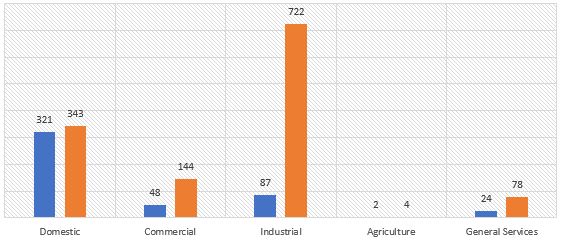

NM consumer growth in Pakistan remained slow until FY2018. By June 2018, NEPRA issued only 460 NM licenses (cumulative), adding 11.4 MW to the country’s installed power generation capacity. However, with increased grid electricity tariffs and falling solar PV costs, NM jumped in FY2021 (Figure 2).

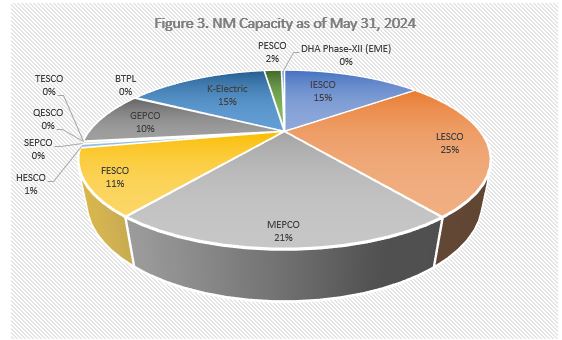

As of June 30, 2023, the number of NM-based solar installations had reached 63,703 with a cumulative capacity of 1055.03MW. By the end of May 2024, the capacity had more than doubled to 2188 MW, spread across 145,537 consumers of all categories. LESCO leads, followed by MEPCO and IESCO (Figure 3).

Source: NEPRA State of Industry Report (Various Years) and PPIB

Source: PPIB

4.4. Net-Metering and DISCOs Concerns

With the growth in NM consumers, DISCOs are showing concerns about financial loss and technical challenges.

Financial Loss

The capacity payments of contracted plants on take-or-pay, recovered through consumer tariffs, are piling up because of the underutilization of grid electricity. DISCOs owe this to NM consumers. Pakistan’s power sector is undoubtedly under the burden of capacity payments. Capacity payments for FY2023 were PKR 1.95 trillion, which increased to PKR 2.1 trillion in 2024. In the electricity tariff for FY2024, consumers paid PKR 16.22/kWh as capacity charges.

DISCOs are raising the issue of fairness without substantial evidence. It is argued that poor consumers without a net-metering facility are subsidizing wealthy consumers with net-metering. While this may be a concern in the future, currently, there is no such impact.

During FY2023, the total sanctioned load for DISCOs was 104,636.7 MW, and the total installed NM capacity was 1055 MW. With a plant factor of 18%, the maximum PV generation could be 190 MV, which is 0.18%[13] of the total sanctioned load—too low to have any impact.

- In actuality, as per NEPRA State of Industry Report 2023, in FY2023, the electricity procured by the distribution companies was 125468GWh. The NM consumers with photovoltaic (PV) systems contributed 183 GWh, just 0.12% of total electricity procured (Table 1). Hence, NEPRA’s February 10, 2023, decision that rooftop solar generators share less than 1% of the country is still valid[14].

- In FY2024, the electricity procured by the distribution companies was 124,861 GWh (NEPRA Tariff Determination, July 14, 2023). Let’s assume that during FY2024, NM consumers’ contribution to the grid more than doubled to roughly 400 GWh. Still, its share will be less than one (i.e., 0.32%) of total electricity procured.

The literature suggests that the costs and problems attributed to NM would not exist in utilities where energy demand is growing (SAARC, 2021). However, in Pakistan, energy demand has started decreasing, increasing the capacity payment burden for the remaining consumers.

The utilities’ claim that the increasing number of NM consumers is the main cause of the decreasing demand is inaccurate. During FY2023, NM consumers exported 482GWh of electricity, while the overall demand decreased by 10,528GWh. The reluctance of DISCOs to acknowledge the impact of commercial load shedding, particularly in loss-making areas, on the decrease in demand, is a significant oversight.

Many parts of the country experience load-shedding for up to 12 hours or more, driving consumers away from the grid. Furthermore, an increase in electricity tariffs due to DISCO inefficiencies and rising capacity payments from the new take-or-pay capacity is driving consumers, especially the industry, away from the grid.

DISCOs are not making any efforts to increase their sales. During FY2023, many eligible consumers were still waiting for connections. By the end of FY2023, 275,267 applications were pending with DISCOs despite fulfilling all formalities (NEPRA Performance Evaluation Report for Distribution Companies, 2023). Not providing timely connections led to a load that could not be integrated into the national grid. Hence, missed opportunities for sales growth and reduced capacity payments per unit, ultimately leading to lower consumer tariffs.

Further, during FY2023, 0.19% of the total grid-connected consumers had a net-metering connection. 481,863,365 kWh were exported against the import of 1,290,872,894 kWh—almost 2.67 times more units were imported during FY2023 (excluding K-Electric) (Figure 4).

Source: NEPRA State of Industry Report 2023

- In FY2023, these consumers exported at PKR 19.32/ kWh (PPP) while imported in peak hours roughly at PKR 33.8 /kWh and in off-peak hours at PKR 27.5/kWh more than the PPP. These consumers import mainly at the time when solar power is not available. The higher peak and off-peak rates for imported units indicate that these consumers (prosumers) are already contributing to the fixed costs of the capacity (which utilities procure to supply nonstop electricity to all grid consumers) and for other system inefficiencies. The net amount paid by these consumers for the imported units in hours when solar PV is not available was PKR 27.8 billion (Table 2).

- In FY2024, these consumers exported units at the rate of PKR 22.9/KWh (PPP) while importing units at the rate of PKR 41.89/KWh in peak hours and at PKR 35.57/KWh in off-peak hours. The net amount paid by NM consumers for FY2024 is expected to be PKR 73 billion (Table 2).

- So, the apprehension that NM consumers are being subsidized by consumers without NM is currently incorrect. However, as the capacity payment burden increases, this could be of concern in the future.

Table 2. Impact of NM incentive

| FY2023 | FY2024 | |

| Average Unit Rates for NM Imports | Peak = PKR 33.8/kWh Off-peak = PKR 27.5 /kWh | Peak = PKR 41.89/kWh Off-peak = PKR 35.57 /kWh |

| NM Export Unit Rate | PKR 19.32/kWh | PKR 22.9/kWh |

| Total units Imported | 1,290,872,894 kWh | 2,581,745,788 kWh |

| Total units Exported | 481,863,365 kWh | 963,726,730 kWh |

| Assume imported units in peak and off-peak hrs. are in the ratio of 20:80 | ||

| Imported Units in Peak hrs. | 258,174,579 kWh | 516,349,158 kWh |

| Imported Units in Off-peak hrs. | 1,032,698,315 kWh | 2,065,396,630 kWh |

| All Prosumers Paid in Peak hrs. | PKR 8726.3 million per year | PKR 21,629.9 million per year |

| All Prosumers Paid in Off-peak hrs. | PKR 28,399.2 million per year | PKR 73,466.2 million per year |

| Prosumers Received at PPP | PKR 9,309.6 million per year | PKR 22,069.3 million per year |

| Net Balance Paid (Import – Export) | PKR 27,815.9 million per year | PKR 73,026.8 million per year |

Source: Author’s Estimates (data source is NEPRA(2023) and GIZ (2024). Note: Actual data on exported and imported units for FY2024 is not available. Here we assume that exported and imported units doubled in a year.

A reason behind DISCOs resistance to NM is the revenue lost due to decreased electricity sales to three-phase consumers. This doesn’t seem correct for the domestic sector at the aggregate level. The total consumption of TOU or three-phase domestic consumers was almost similar between 2020 and 2023[15]. Although this is not a very good parameter, it is just to have an idea.

Table 3. Electricity Consumption by Three-phase Residential Consumers (GWh)

| 2020 | 2023 | |

| Peak Consumption | 520 | 501 |

| Off Peak Consumption | 2135 | 2169 |

| Total | 2655 | 2670 |

Source: NEPRA Tariff Determinations 2020 and 2023

Another misconception is that NM consumers are subsidized if their net import units are less than 200 kWh, which is incorrect. NM consumers are three-phase consumers; a progressive slab tariff is not applied to them.

Technical Concerns

DISCOs believe that due to increased solar PV connections (NM), reverse power is observed on distribution transformers. According to GIZ(2024), reverse power flow can occur only in March, April, October, and November. During peak summer months, most of the energy generated is self-consumed. However, in the winter months, energy generation from solar PV systems is reduced due to fog and low irradiation levels in most of the geographical areas of Pakistan. The report also suggests installing a transformer monitoring system and enabling warning alarms for high reverse power flow can help reduce transformer burnout.

It’s a fact that NM consumers are increasingly exporting units to DISCOs (Table 4). These consumers are using the grid to store the electricity their roof-top solar PV is generating[16]. If the trend continues, it could lead to serious technical[17]and financial challenges in the future. Some customers have surpassed the specified limit by installing too many solar panels on their NM connections, causing unauthorized energy feedback. This has led to power quality and overvoltage issues during low demand.

According to NEPRA guidelines, the distribution company has the authority to monitor and act in such cases, but DISCOs have failed to do so. No mechanism or monitoring system is in place to judge whether the installed capacity has crossed the prescribed limit.

Table 4. NM Exports and Imports (kWh)

| Exports per Consumer | Imports per Consumer | |

| FY2022 | 3,989.2 | 23,022.3 |

| FY2023 | 8,539.6 | 22,876.9 |

Source: NEPRA State of Industry Report 2022 and 2023

Despite the growing emphasis on RE over the past decade, DISCOs have not upgraded or modernized their systems. Even though some DISCOs have conducted GIS mapping, the lack of hosting capacity analysis (HCA) [18] is a significant concern. They don’t have a dedicated department to monitor the real-time injection of PV power, and the monitoring of installed DG capacity has never been done. The absence of a real-time platform to analyze the real-time injection of PV power in the grid is a worrying issue (GIZ, 2024).

Several countries, like India and Germany, are moving towards AMI. But in Pakistan, it has yet to be implemented. AMI allows for better oversight of actual network management capacity. Furthermore, state-owned DISCOs have not implemented SCADA systems.

5. Way Forward

Integrating RE by harnessing solar potential and adopting NM has revolutionized the energy landscape globally. Along with the changing electricity system and technology, NM policy and supporting regulations have been evolving. Yet, reasonable protection is provided to existing consumers. Similar advances can be made in Pakistan’s energy sector.

Changes to financial incentive schemes in Pakistan should happen only after necessary infrastructure upgrades and regulatory revisions. All stakeholders must critically evaluate the formulation and implementation of any change in the current NM regime.

The RE in Pakistan has suffered from inconsistency in policy all along. For its widespread adoption, effective policy formulation, including legislative enactments, financial incentives, and developing an effective tariff structure that promotes efficient energy use, can help.

- Regulatory amendments are required to allow pre- and post-installation inspection to ensure compliance and safe operations under NM. Periodic load flow studies are necessary in areas with high solar PV penetration (Tahir et al., 2023 and GIZ, 2021).

- DISCOs must prioritize installing transformer monitoring systems and enabling warning alarms to reduce the transformer burnout ratio in case of high reverse power flow.

- DISCOs must conduct hosting capacity analyses (HCAs) of their networks to understand their capability to integrate solar PV.

- If the capacity a feeder can accommodate without changes is known in advance, there will be no adverse impacts; thus, no reinforcement or upgrades will be needed.

- A portal can be established to monitor NM energy production and consumption, providing real-time data. A dedicated RE department consisting of RE experts must be established at the DISCO level (GIZ, 2024).

- Unauthorized NM connections/ limits must be dealt with according to NEPRA-approved regulations and guidelines, ensuring that all installations comply with legal and safety standards.

- Limit the solar roof-top maximum capacity equal to the sanctioned load.

- DISCOs should simplify new connection processes, invest in infrastructure, and coordinate with stakeholders to minimize delays. This will increase electricity demand, spread the capacity payment burden, and enhance consumer convenience.

- Frequent media speculation about NM policy/regulations changes continuously threatens existing consumers. To avoid confusion for consumers and the solar industry, precise cut-off dates for the current NM system should have been set.

- Integrating battery storage along with NM to meet the peak load of customers must be made mandatory through regulatory amendments. NM benefits in Italy outweigh the energy storage systems; storage alone was economically unsustainable.

- Over 90% of NM connections serve personal consumption needs. When combined with battery storage, consumers will primarily use their own electricity, transferring only a minimal amount of excess.

- All NM connections must have a remote disconnection facility via AMI with decentralized (utility) control for grid safety.

According to reported data, distribution losses were 22286 GWh in FY2023 (unofficial sources suggest the actual figure is much higher). It is much higher than the NM exported units in FY 2023 (482 MW). The financial impact of distribution losses is quite significant, approximately translating to PKR 734 billion. NM electricity experiences zero line loss, thereby assisting DISCOs in reducing their line losses.

- Addressing distribution losses should be the primary focus of distribution companies.

- AMI not only helps to monitor grid safety but can also be an effective instrument for controlling non-technical losses (theft) in the distribution system.

Source: NEPRA State of Industry Report 2023

In Pakistan, despite being trapped in a capacity dilemma, decision-makers are more focused on increasing the capacity of solar IPPs. In contrast, rooftop solar allows for small private investments without the burden of capacity payments or exposure to fluctuations in the dollar exchange rate. This helps reduce carbon footprints and lessen the strain on public funds, thereby promoting a sustainable, self-sufficient energy environment. Even more importantly, rooftop solar does not require new transmission infrastructure.

Our current transmission system can only handle the evacuation of 25950 MW out of the total installed capacity of 43749 MW. As a result, 17799 MW of capacity remains idle, and we are still paying for their capacity. This has a much more significant impact than the NM impact. Additionally, large-scale solar IPP also involves an unviable and expensive transmission evacuation system.

Merely following global trends and setting ambitious targets for energy transition is insufficient. Addressing ground realities to provide the enabling environment for transition is essential. NM benefits consumers by helping to reduce electricity bills and contribute to a sustainable energy future. If managed properly, it allows for diversified power supply sources, reduced peak-hour electricity demand, and improved grid stability. This helps mitigate strain on utilities and decreases power losses in long-distance transmissions. Above all, clean energy generation methods, such as solar PV (on-grid or off-grid), can generate carbon credits.

After necessary upgrades, NM-based generation units can alleviate financial burdens and provide a cost-effective solution. Investing in modernizing the grid is crucial to ensure that all customers, not just the prosumers, can fully benefit from these changes.

References

- Abdin, G. C., & Noussan, M. (2018). Electricity storage compared to net metering in residential PV applications. Journal of Cleaner Production, 176, 175-186.

- Australian PV Institute [APVI] Solar Map, funded by the Australian Renewable Energy Agency [ARENA]. (Accessed 2024, July 4). Retrieved from pv-map.apvi.org.au

- Cordeiro, I., Bassi, W., and Sauer, I. L. (2023). Hosting Capacity Estimate Based on Photovoltaic Distributed Generation Deployment: A Case Study in a Campus of the University of São Paulo. Energies, 16, 3934.https://doi.org/10.3390/en16093934.

- GIZ (2021). Tecno-Economic Assessment of Single-Phase Net-Metering. Report by Intec Group under Integration, Environment and Energy. GIZ (Deutsche Gesettschaft fur Internationale Zusammenarbelt (GIZ) GmbH.

- GIZ (2024). Net Metered Distributed Generation: Challenges, Solutions and Way Forward. Published by Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) GmbH.

- Karthik, M. (2023). Understanding Solar Net Metering for Consumers in India. https://cdn.cseindia.org/attachments/0.52095900_1685525460_understanding-solar-net-metering-for-consumers-in-india.pdf

- Klein, C. (2024, February 12). Share of renewables in electricity generation Japan FY 2013-2022. Retrieved from https://www.statista.com/statistics/745908/japan-share-of-renewables-in-electricity-production/

- Max Staib Ramalho, M. S., Câmara, L., Pereira, G. I., Silva, P. P., and Dantas, G. (2017). Photovoltaic energy diffusion through net-metering and feed- in tariff policies: Learning from Germany, California, Japan and Brazil. Center for Business and Economic Research, Faculty of Economics, University of Coimbra.

- National Academy of Sciences (2023). The Role of Net Metering in the Evolving Electricity System. https://www.nationalacademies.org/our-work/the-role-of-net-metering-in-the-evolving-electricity-system

- National Electric Power Regulatory Authority. (2022). State of industry report 2022

- National Electric Power Regulatory Authority. (2023). State of industry report 2023.

- SAARC (2021). Study on Technical Issues and Financial Viability of Net-Metering Mechanisms Perspective of Distribution Utilities. Published by SAARC Energy Centre, Islamabad, Pakistan.

- Tahir, M., Siraj, K., Shah, S., & Arshad, N. (2023). Evaluation of single-phase net metering to meet renewable energy targets: a case study from Pakistan. Energy Policy, 172, 113311. https://doi.org/10.1016/j.enpol.2022.113311

- Uibeleisen, M., & Groneberg, S. (2024, April 29). Solar Package 1: Overview of the Main New Solar Regulation in Germany. Retrieved from https://www.mwe.com/insights/solar-package-1-overview-of-the-main-new-solar-regulation-in-germany/

- Yuen, S. (2024, March 21). Japan announces feed-in tariffs for residential and C&I PV systems. PV Tech. Retrieved from https://www.pv-tech.org/japan-feed-in-tariffs-2024-2025/

[1]This sub-section relies heavily on information available on https://www.maxpower.com.pk/news/overcoming-net-metering-challenges-solutions-for-a-smoother-transition/

[2]https://www.mordorintelligence.com/industry-reports/solar-energy-market?network=g&source_campaign=&utm_source=google&utm_medium=cpc&matchtype=p&device=c&gad_source=1&gclid=Cj0KCQjw9vqyBhCKARIsAIIcLMECnk1YKr4iOQ5w4TTMA8QS_-lfBvrd7RpwuPRCZ68EEVUEoJlSrSgaAoQ5EALw_wcB

[3]In the USA, the NM facility is available in 38 States, mandatory in several among them; where no NM, storage is the only option for DG.

[4]Japan was the first Asian country to introduce the NM policy.

[5]The Grid Feed-In Law was passed in 1991 and replaced by the Renewable Energy Sources Act in 2000.

[6]Solar PV installations reached 3.76 million, with a cumulative capacity of 35.6 gigawatts (Australian PV Institute [APVI] Solar Map).

[7]It can even exceed 100% if aligned with peak grid loads or two RE technologies used under NM have complementary generation patterns.

[8]Inverters used in rooftop solar systems must now be capable of adjusting their output in response to grid frequency changes.

[9]https://caneurope.org/content/uploads/2024/04/Germany-Residental-Rooftop-Solar-Country-Profile.pdf

[10]https://www.marketwatch.com/guides/solar/solar-net-metering/

[11]https://blogs.nicholas.duke.edu/env212/residential-solar-net-metering-policies-in-the-united-states-navigating-the-transition-to-a-sustainable-future/

[12]Industrial Captive Solar stands at about 1000MW (rough estimate), and this number is evolving.

[13]In IGCEP (2023-24), the capacity factor for net metering is 18%.

[14]NEPRA Ruling (February 10, 2022) states, “…net metering is predominantly based on the concept of minimizing the electricity cost through roof top solar self-generation for self-consumption and not for commercial sale and DISCOs have to maintain Grid & Generation Capacities for the Net Metering Consumers during non-solar hours as well. However, at the same time the economic benefits of net metering in terms of displacement of costlier electricity, savings of foreign exchange and incurring minimal losses, cannot be ignored. Moreover, the quantum of net metering units, at present is very low i.e. below 1% of the total energy purchased by DISCOs.”

[15]Exact number of TOU residential consumers is not available in publicly available reports.

[16]At the end of each three-month cycle, surplus units are converted to monetary value and deducted from the peak unit consumptions. This significant financial incentive is a key factor encouraging NM consumers to install more solar capacity than they currently need.

[17]When electricity exporting units go beyond the distribution transformers’ capacity, they reduce the life of the equipment and increase 11kV losses.

[18]HCAs provide greater transparency into the grid. It can help reveal the grid’s operational limits, which impact the new DG’s ability to interconnect quickly or affordably. It can also identify areas where DG may provide beneficial services by addressing existing grid constraints and informing more strategic grid investments over the long term (Cordeiro, et al., 2023).